Liquidity is a key component when it comes to analyzing a company’s financial health. It allows the company to meet its short-term obligations with the assets it has available. And when it comes to running a successful business, cash flow and liquidity aren’t just metrics–they’re the lifeblood of the organization.

The cash conversion cycle is one of the most powerful (and most overlooked) financial tools available to business owners and their advisors. Despite its remarkable potential, it has been consistently underutilized. That’s a mistake worth correcting.

If you’ve read our other articles, such as how a 13-week cash flow model can benefit your business, you know that we are big believers in companies using cash forecasting as a management tool. In this article, we discuss how companies can use the Cash Conversion Cycle (CCC) as an analysis tool to improve their cash flow and working capital utilization.

What Is the Cash Conversion Cycle?

Traditional liquidity ratios provide a snapshot of a company’s short-term financial strength. The current ratio (current assets divided by current liabilities) and the quick ratio (cash & equivalents + marketable securities + accounts receivable divided by current liabilities) are the staples of these assessments.

These ratios give a simplified perspective of a company’s ability to cover its immediate liabilities with readily available assets. However, they lack the depth to capture the dynamics of cash flows and the time it takes for a company to convert its resources into cash.

The CCC, introduced in 1980 by Verlyn Richards and Eugene Laughlin, is a dynamic approach that brings the element of time into the equation. It recognizes that the process of converting raw materials into finished goods, selling them, and ultimately receiving cash involves several stages, each with its own unique time frame. The result is a more comprehensive assessment of a company’s liquidity position.

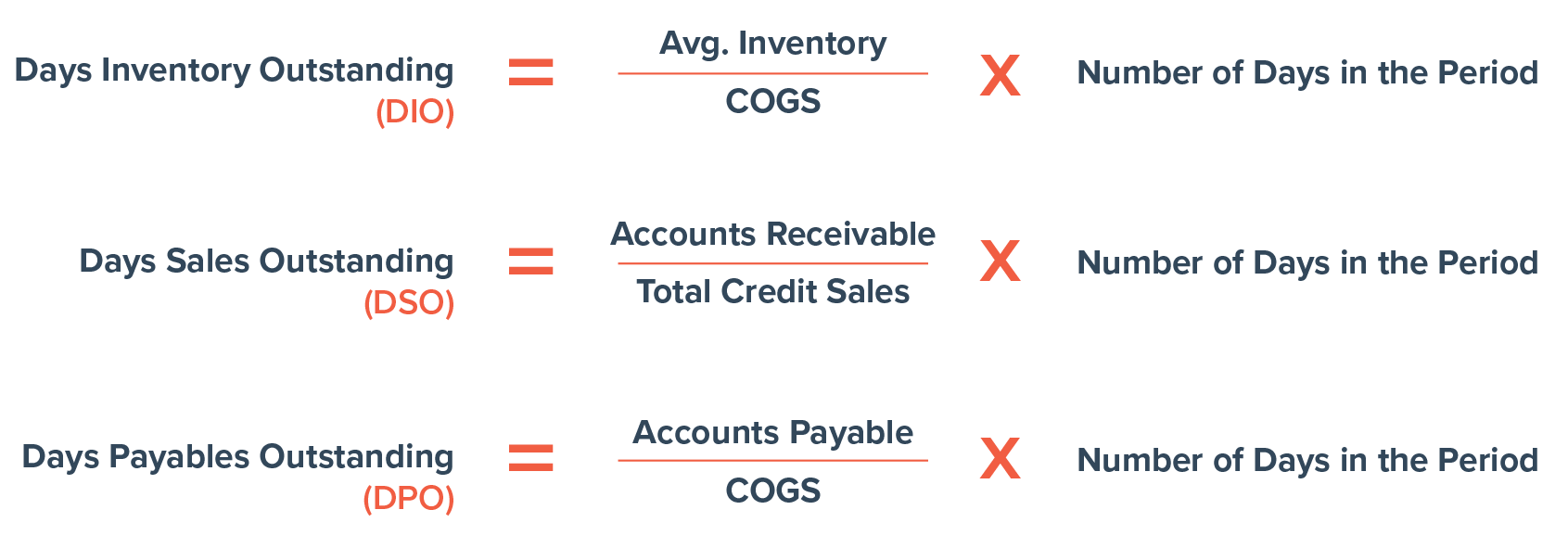

There are three key time-measuring components involved in the cash conversion cycle to determine how long it takes for a company to convert its investment in inventory and other resources back into cash through sales:

- Days Inventory Outstanding (DIO): This represents the average number of days it takes for a company to sell its inventory. A lower DIO implies more efficient inventory turnover and quicker conversion of inventory into sales.

- Days Sales Outstanding (DSO): DSO indicates the average time it takes for a company to collect payments from its customers after a sale. A shorter DSO signifies better credit and collection policies, leading to faster cash inflows.

- Days Payables Outstanding (DPO): DPO measures the average time a company takes to pay its suppliers. Extending payment terms can provide a source of short-term financing, resulting in longer cash outflows.

To calculate the CCC, subtract DPO from the sum of DIO and DSO: CCC = DIO + DSO − DPO.

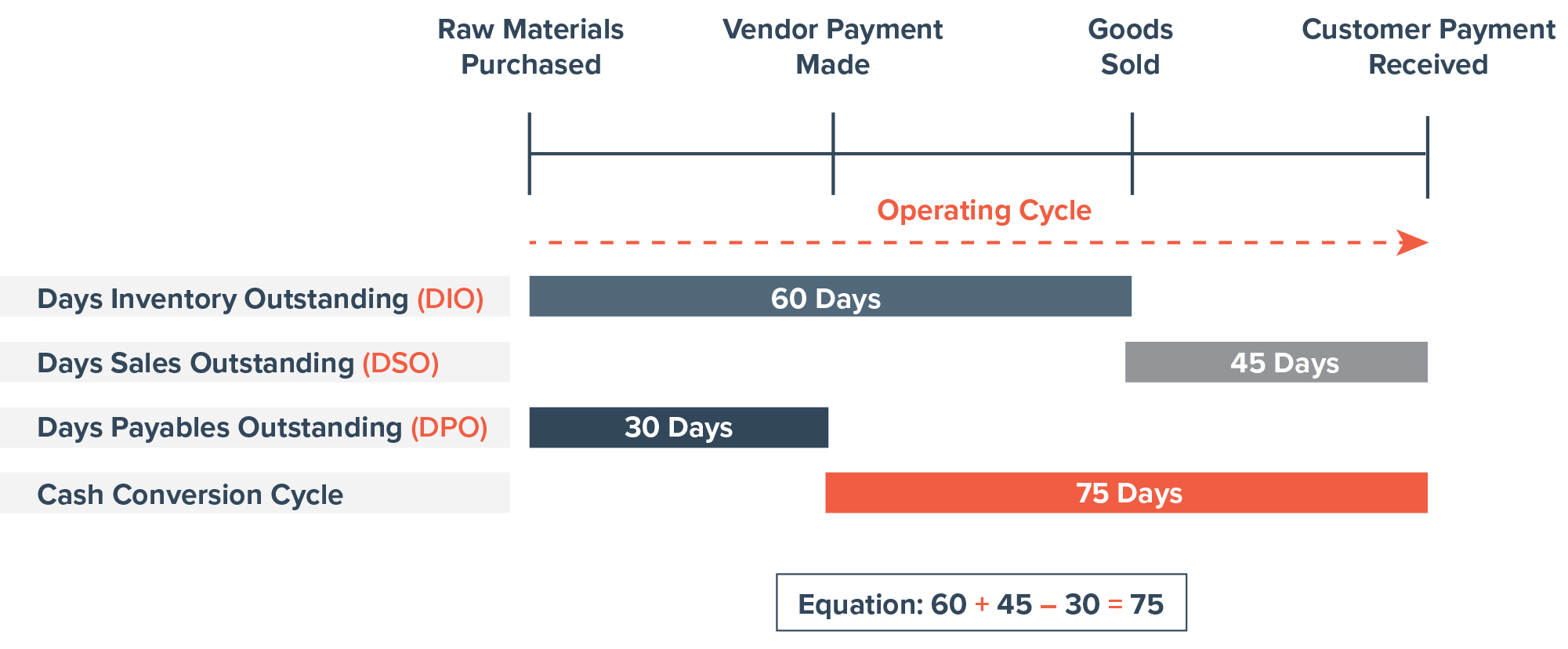

The diagram above illustrates how the three components combine to produce the CCC. In this example, a company with 60-day inventory turnover, 45-day collections, and 30-day payables has a cash conversion cycle of 75 days–meaning it takes 75 days from the time cash goes out to buy inventory until it comes back in from customer payments.

The formulas above show how each component is calculated. These inputs come directly from a company’s financial statements, making the CCC a straightforward but powerful addition to any financial analysis.

So, while traditional liquidity ratios provide valuable insights into a company’s immediate financial standing, the fact that they don’t account for the element of time creates a gap that the CCC fills. By considering the cycle alongside traditional ratios, business leaders and analysts can gain a more thorough understanding of a company’s operational efficiency, cash flow management, and potential liquidity risks.

Benefits of the Cash Conversion Cycle

Think of the CCC as a heart monitor for your company’s financial health. It measures a company’s net investment in working capital and offers a dynamic picture of how efficiently that capital is being put to work.

Here’s what it can do for your business:

- Operational Efficiency. A shorter CCC signifies streamlined operations, efficient inventory management, and swift conversion of resources into cash.

- Cash Flow Management. By identifying areas where cash is tied up in the operating cycle, a company can devise strategies to optimize cash flow and reduce the cycle time.

- Risk Assessment. CCC analysis highlights potential liquidity risks that may arise due to delays in inventory turnover, slow collections, or unfavorable payment terms.

- Comparative Insights. CCC allows for meaningful comparisons between companies in similar industries, enabling business leaders, investors, creditors, and analysts to assess how different operational strategies impact liquidity.

- Informed Decision-Making. Business leaders and investors can make more educated decisions by considering a company’s operational efficiency and liquidity position through the CCC lens.

- Strategic Guidance for Advisors. Business advisors leveraging CCC insights can offer targeted guidance to enhance working capital management for their clients, making it a particularly valuable tool in a working capital consulting engagement.

How to Improve Working Capital Using the CCC

The CCC gives you a clear starting point for how to improve working capital. It’s not just a diagnostic tool–it’s a roadmap for improvement. Once you understand where cash is getting “stuck” in your operating cycle, you can take targeted action.

Focus on three levers:

- Reduce DIO by tightening inventory management and improving turnover rates.

- Shorten DSO by improving collections processes and tightening credit terms.

- Extend DPO where possible by negotiating better payment terms with suppliers.

Each lever you pull moves the CCC in the right direction and puts more cash back in your business. It’s not just a tool. It’s a perspective shift. For business leaders, the CCC provides a more educated view of how cash is moving through their business, or in some cases, where it’s getting stuck.

Considering Working Capital Consulting?

At JACO, we’re not consultants–we’re advisors who think like business owners. We can help you calculate your CCC, benchmark against industry peers, and identify real opportunities to improve working capital and cash flow. Contact our experienced team today to discuss how the cash conversion cycle can improve your working capital and cash flow.

About Jeff

Jeff has over 30 years of strategic planning, business development, and business transformation leadership experience. Having worked with mid-market, closely-held and family-owned businesses his entire career Jeff has a unique understanding of how these enterprises operate and the challenges they face.

He is passionate about working with business leaders to build strong cultures while developing and executing strategies that deliver exceptional results that benefit all the company’s stakeholders. Jeff’s hands-on approach to working with companies begins with a commonsense approach to strategy development.

With extensive experience in organizational turnaround and growth Jeff follows a defined process (disciplined, focused, intentional) to guide clients from strategy to execution. His experience covers a multitude of industries, with an in-depth understanding of automotive manufacturing.

Jeff holds a Master’s in Business Administration from the Capital University School of Management and earned a Bachelor of Arts in Business Administration and Management from Ohio Dominican University.

He is a Certified Turnaround Professional (CPT) by the Turnaround Management Association and is a Certified Exit Planning Advisor (CEPA) by the Exit Planning Institute.